There is a pattern I have seen repeat itself across three decades in the fitness, sports nutrition, and healthy snack markets. A founder builds something that works. A real product solving a real problem for consumers willing to pay for it. Velocity builds, trust builds, and the brand starts to mean something in the market. Then, instead of going deeper into what’s working, they start launching sideways.

New categories. Unrelated audiences. Tangential formats that share no equity with the product that earned the brand its position in the first place. The calendar stays full and the portfolio gets bigger — but the clarity that made the original product worth paying attention to slowly dissolves.

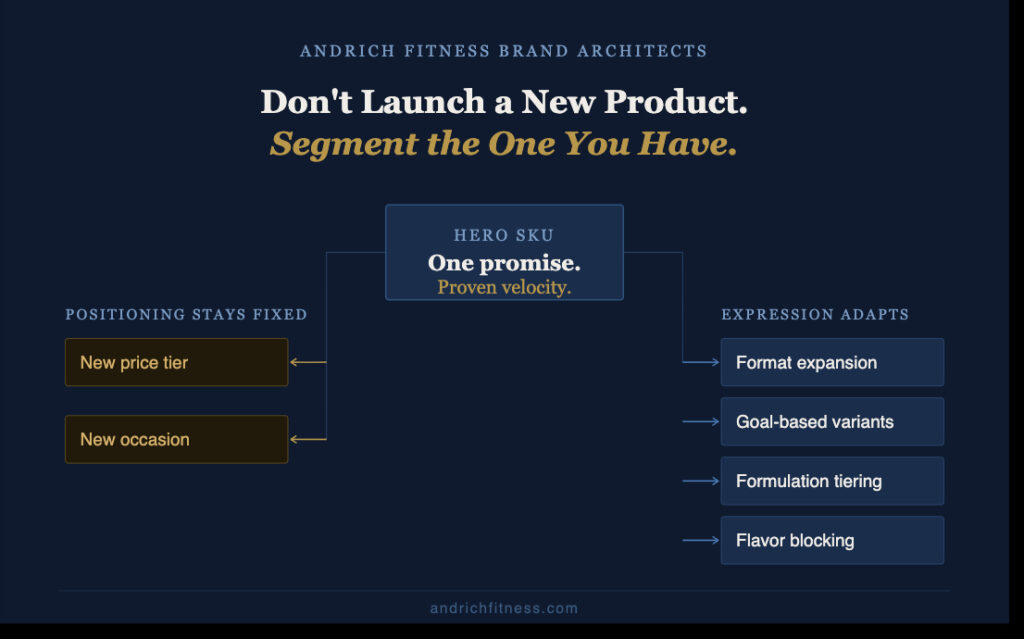

The brands that actually compound do the opposite. They don’t launch outward. They launch inward. They go deeper into the hero SKU they already have — and they do it through segmentation.

A successful product is solving a real problem. That problem has more than one version.

A product earns real velocity because it solves a real problem and delivers a real, felt benefit. Not a vague wellness promise — a specific outcome a specific consumer experiences. That specificity is not a limitation. It is the source of the segmentation opportunity.

Because the consumer who has that problem is not one person. They are a spectrum of people with adjacent versions of the same problem, each with a slightly different goal, training approach, lifestyle constraint, or consumption occasion. The hero SKU speaks powerfully to one expression of that problem. Segmentation extends that same credibility to the rest of the spectrum.

Athletic Greens AG1 is as close to a universal positioning as the supplement category has produced — everything you need in one scoop for the consumer who wants comprehensive daily nutrition without managing multiple products. Genuinely rare, and it’s why AG1 has scaled the way it has. But even AG1 follows the same logic eventually. An RTD doesn’t change the positioning. It puts the same promise into a new consumption occasion. The scoop becomes a bottle. The positioning never moves. The access point does.

The governing idea

Every segmentation decision worth making starts from the same fixed point: a master positioning that does not move.

C4 started with a single, tight master positioning: explosive pre-workout energy for serious training. One product, one promise, sold almost exclusively through GNC. The name itself was the message — military-grade explosive power, detonated in the gym. Clean, ownable, and immediately credible.

Huel started from an equally clear position: nutritionally complete food that fits your life. One powdered meal, one promise — a complete meal in a shake, plant-based, designed for busy people who want to eat well without the time or friction of cooking. No performance angle. No gym required. Just complete nutrition, made simple.

In both cases, the master positioning is constant. What changes across variants is the specific expression of the goal being served, the format being used, the price point being addressed, and the consumption occasion being unlocked.

That is the precise distinction between segmentation that compounds a hero and extension that dilutes it. Segmentation keeps the master positioning fixed and adapts its expression to adjacent consumer needs within the same category. Extension moves the master positioning itself into new territory the brand has not yet earned the right to own.

A pre-workout brand launching a protein bar is extension. A pre-workout brand launching a stimulant-free variant for consumers who train at night is segmentation. One borrows from the hero’s equity. The other deepens it.

Segmentation keeps the master positioning fixed and adapts its expression to adjacent consumer needs. Extension moves the positioning itself — into territory the brand hasn’t yet earned.

How C4 built the category from the inside out

C4’s ascent to the #1 pre-workout brand in the US is the clearest modern example of segmentation executed as a market capture strategy — and it happened in four distinct stages.

Stage 1 — The Hero SKU. One product. One promise. Specialty retail.

C4 Original launched with a positioning that was almost blunt: explosive pre-workout energy for serious training. The beta-alanine tingles were marketed as proof it was working. The GNC relationship gave it immediate specialty retail credibility. There was nothing complicated about it — and that was exactly the point.

Stage 2 — Segmentation: Wide and Deep. Goal-based variants + formulation tiering.

Rather than launching outside the category, Cellucor went deeper into it — building variants across two axes simultaneously:

- Training type: Original → Sport → Ripped → Extreme → Ultimate. Each variant addressed a specific consumer goal — athletic performance, fat loss, high-stim intensity, fully-loaded clinical dosing — while drawing from the same master brand.

- Price point: Entry-accessible at the bottom, fully-loaded premium at the top. A true good/better/best architecture that owned multiple shelf facings while justifying higher ASPs at the top of the ladder.

Stage 3 — Earned Repositioning. The segmentation creates permission the original SKU never had.

Once the product architecture actually served every athlete, C4 earned the right to a broader claim: “The pre-workout for every sport, every training style, every goal.” That positioning was not available on day one. No brand can credibly claim to serve everyone before it has built the proof. The segmentation built the proof. The repositioning just named it.

Stage 4 — Scale Creates New Markets. Earned expansion beyond the category.

By 2024, Nutrabolt — C4’s parent company — had built enough scale, distribution, and capital from winning the pre-workout category to make a move no pre-workout brand could have made on day one: $90 million for a 20% stake in Bloom Nutrition, the social media–born women’s wellness and greens brand. By September 2025, that investment had grown to over $210 million and a majority stake. Bloom is now projected at $350–400 million in annual revenue.

C4 didn’t buy Bloom because it got bored of pre-workout. It bought Bloom because a decade of segmentation had built the distribution, retail relationships, and financial position to enter a market — women’s wellness, greens, functional beverages — that Bloom already owned. That is earned expansion. And it is a fundamentally different move than launching sideways before you’ve won anything.

How Huel built a meal platform from a single powder

Stage 1 — The Hero SKU. One powder. One promise. DTC-first.

Huel launched with a nutritionally complete meal powder — plant-based, affordable, built for the consumer who wants to eat well without the friction of cooking every meal. The positioning was unambiguous: complete nutrition, made simple.

Stage 2 — Price Point Segmentation Within the Powder. Three tiers. One promise.

Rather than launching new categories, Huel went deeper into its own format:

- Essential Powder: entry-level price point, simplified formula, maximum accessibility.

- Powder: the original standard formula — the hero.

- Black Edition: premium tier, higher protein, lower carb, for the more nutrition-conscious buyer willing to pay more.

Same format. Same occasion. Three different buyers at three different price points. The “nutritionally complete” positioning never moved. The product architecture built the ladder beneath it.

Stage 3 — Format Expansion. The RTD puts the same promise into a new occasion.

Huel’s RTD — available in standard and Black Edition — isn’t a repositioning. It’s the same “nutritionally complete meal” promise in a bottle, for the consumer who doesn’t want to mix a shake at their desk. New occasion. Same promise. The same move I predict AG1 will be making as they expand into physical retail distribution.

Stage 4 — New Occasions, Same Master Positioning. Hot & Savory completes the day.

Huel’s Hot & Savory Meal Packs and Cups are arguably the most instructive move in the Huel story. On the surface they look like a category extension. They are not. The promise is identical: nutritionally complete food that fits your life. What changes is the occasion — a hot lunch at a desk, a fast dinner after a long day. The positioning never moved an inch. The consumption window expanded to cover the whole day.

This meal supplement segmentation playbook isn’t new. At EAS, we ran the same play with Myoplex — starting with a single MRP powder and building out Deluxe, HP, Lite, and Mass variants to serve different goals and price points, then extending into bars and RTDs to expand the consumption occasion. Through all of it, the “precision nutrition for serious athletes” positioning never moved. The format changed. The goal segment changed. The brand promise didn’t. The full Myoplex segmentation story — and what it teaches about building a meal platform before the market was ready to call it that — is coming in a future piece.

The four moves that work

Across the brands I have worked with directly, four segmentation tactics show up repeatedly when a hero SKU is being built into a platform.

Format expansion takes the core product into new consumption occasions without changing its fundamental promise. Huel’s RTD and Hot & Savory lines are the current benchmark.

Goal-based variants adapt the foundational formulation for consumers with slightly different outcomes in mind, turning the hero into the answer for an entire consumer spectrum. C4’s training-type architecture — Original through Ultimate — is the definitive modern execution.

Flavor blocking is a retail strategy as much as a product strategy. Expanding variety within a single format occupies more facings, reduces a competitor’s ability to gain shelf space, and makes a brand the most important player in its category at a given account. (Quest Nutrition built this model at specialty retail before moving to FDM — a full breakdown is coming.)

Formulation tiering builds a ladder of options calibrated to different consumer goals, price tolerance, or intensity levels — making the brand the complete answer to the category. Huel’s Essential–Powder–Black Edition structure and C4’s Original–to–Ultimate architecture are two of the cleanest current executions.

What the market data says

According to SPINS data tracking the powder and supplement category, C4 holds the #1 position in pre-workout in US MULO — and Bucked Up runs a close second. Both brands built their positions the same way: tiering their core pre-workout formulations across consumer goals and stimulant tolerances rather than launching outside the category. Every consumer in the pre-workout aisle, regardless of goal or sensitivity level, can find their version. Competitors got squeezed out not because they had worse products, but because they had less real estate in the consumer’s decision set.

Note: SPINS pre-workout data reflects the powder and supplement category. C4’s RTD energy business — expanded into convenience, grocery, and mass retail — is a separate, significantly larger revenue story. The RTD didn’t create the brand. The brand made the RTD possible.

Segmentation only works when the positioning does its job. A higher-dose variant sitting next to a standard formula is not segmentation — it is a dosing option. Each variant needs to position clearly to a specific use case: Daily Use. Strength. Hypertrophy. Endurance. The tangible difference in the formula has to connect to a tangible difference in the consumer’s mind. Without that, the brand has added complexity without adding clarity — which is the opposite of what segmentation is supposed to do.

The channel dimension

Segmentation tactics are not channel-agnostic. The move that builds category dominance in MULO is not always the right move in DTC or specialty retail.

Retail rewards formulation tiering and goal-based variants — more facings, clearer merchandising logic, stronger buyer conversations. Specialty retail rewards goal-segmented variants because the sales associate conversation is built around consumer outcomes. DTC and Amazon reward flavor variety and format options that increase basket size and drive repeat purchase. Club rewards format expansion into value configurations that create incremental volume without cannibalizing the core.

The right segmentation move is always specific to where the brand is actually building its business right now — not where it might operate someday.

Why founders resist this — and what it costs them

The most common objection to segmentation is that it will dilute the hero — that a variant will confuse the consumer, cannibalize the original, or weaken the brand’s clarity of purpose. I have heard this argument made sincerely by smart people at real brands, and in some cases watched it prevent growth that was sitting directly in front of them.

The objection is not entirely wrong. Poorly executed segmentation can create confusion. A variant that sends a contradictory message, targets a misaligned consumer, or lands in the wrong channel can do real damage. But the risk of premature extension is not the same as the risk of under-segmenting, and the distinction matters.

Premature extension is what founders rightfully fear: launching into a new category or audience before the hero SKU has won its market. A $5M brand launching a protein bar because the founder is bored of pre-workout is not segmentation — it is distraction.

Earned expansion is what C4 and Huel are doing at scale. Once a brand has dominated its category — earned the distribution, the retail relationships, the consumer trust, and the capital that category leadership creates — it has the resources and permission to go somewhere new. Nutrabolt didn’t acquire Bloom Nutrition in 2015. It did it after a decade of segmentation built the scale that made a $210 million bet possible. Huel didn’t launch greens and energy drinks first. It built the meal platform first.

The question isn’t whether to ever go beyond your hero. It’s whether you’ve done the work in your core category that earns you the right to go anywhere else.

The practical question

For most founder-led brands, the segmentation opportunity is not a future consideration. It should be actively evaluated right now — against the specific channels the brand is operating in and the specific consumer goals it already has credibility around.

The question is not whether to segment. It is which segmentation move is right for this brand, at this stage, in the channels where it is actually trying to win.

A successful product is already solving a real problem. The only question is how many versions of that problem it should be solving — and how to build the architecture to serve them without losing the clarity that made the hero worth following in the first place.

That question is exactly what the SKU Segmentation Track is built to answer. It starts with your hero SKU, maps the real segmentation opportunity by channel, and builds a prioritized plan for capturing it without diluting what’s already working.

→ Learn more about the SKU Segmentation Track: https://andrichfitness.com/segmentation-track/segmentation-track.html

If you’re not yet confident which product in your lineup deserves to be the platform, the SKU Rationalization Audit is where we start.

→ Find out which SKU deserves your bet: andrichfitness.com/sku-audit

30-minute free discovery call. No pitch. No commitment.